Updated July 2025

Australia’s appetite for Dubai opportunities keeps growing, thanks to world-class free zones, visa reforms, and a maturing real-estate market. Once the returns start rolling in, however, many investors hit the same roadblock: How do I move my Dubai profits back home without triggering unnecessary taxes or compliance headaches?

This guide walks you through the legal pathways, tax considerations, and practical money-transfer solutions available to Australian residents. It is written for:

- Australian shareholders of a Dubai free zone or mainland company

- Individual landlords earning rental income from UAE property

- Entrepreneurs who run their business from Australia but have profits sitting in a UAE bank account

Disclaimer: The information below is general in nature and does not constitute financial or tax advice. Always obtain personalised advice from a licensed Australian tax agent and a UAE-qualified accountant before acting.

1. Map the regulatory landscape first

Transferring money is the easy part. Navigating the two tax systems is what protects your profit margin.

1.1 The UAE side

- Corporate Tax: As of June 2023, most mainland and free zone entities are subject to a 9% federal corporate tax on profits above AED 375,000. Qualifying Free Zone Persons (QFZPs) can still enjoy 0% on eligible income, but they must meet strict substance and reporting rules.

- Withholding Tax: The UAE does not levy withholding tax on dividends, interest, or royalties paid to non-residents.

- Exchange Controls: There are no foreign-exchange controls. Funds can be remitted abroad freely, provided proper KYC/AML documentation is in place.

1.2 The Australian side

- Residence Test: If you are an Australian tax resident, you are taxed on worldwide income, regardless of where the money is held.

- Double Tax Relief: Australia and the UAE do not have a comprehensive Double Tax Agreement (DTA). You may, however, claim a Foreign Income Tax Offset (FITO) for any UAE corporate tax already paid.

- Controlled Foreign Company (CFC) Rules: If you own 40% or more of a UAE company (alone or with associates), its undistributed profits may be attributed to you annually. Timing the dividend matters less than the accounting treatment.

- General Anti-Avoidance Rule (GAAR): Schemes with the dominant purpose of avoiding Australian tax can be unwound by the ATO, even if they were technically legal offshore.

2. Choose the right profit-extraction method

- Dividends

- Cleanest method for company owners.

- Not taxable in the UAE; assessable in Australia in the year you receive them.

- Provide board resolutions, audited financials, and bank advices to satisfy ATO record-keeping rules.

- Management Fees/Service Charges

- Legitimate if you (or an Australian entity you control) actually provide services to the UAE company.

- Must be priced at arm’s length to avoid transfer-pricing adjustments.

- Salary or Director’s Fees

- Subject to UAE personal income tax? Currently 0% (there is no PIT). In Australia, taxed upon receipt but may attract superannuation obligations if you are an employee of your Australian business.

- Property Rental Surplus

- Landlords can remit net rental income monthly or quarterly.

- Attach the Ejari (tenancy) contract, DEWA bills, and Form NR (non-resident landlord) declarations if the property is managed by a third party.

- Capital Repayments

- On selling a Dubai property, capital gains realised in the UAE are still taxable in Australia. Keep the sales contract (Form F), No Objection Certificate (NOC) from the developer, and security cheque releases.

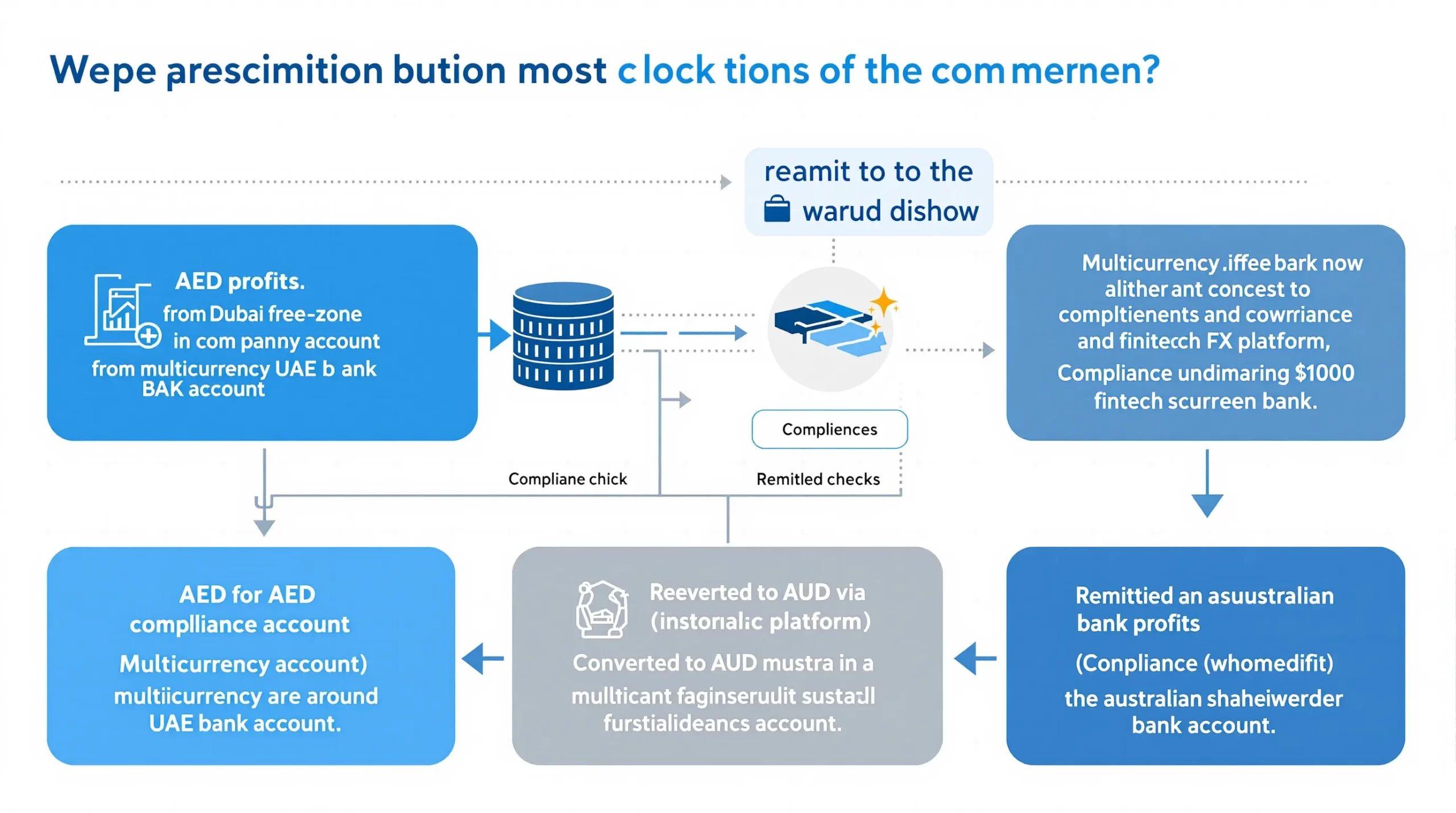

3. Set up compliant banking rails

- Open a multicurrency corporate account in the UAE (Emirates NBD, Mashreq NEO Biz, or WIO are popular with foreigners). Holding both AED and USD reduces conversion spreads.

- Link a personal or holding-company account in Australia that can receive large international SWIFT payments. A bank that offers an AUD-denominated IBAN (Macquarie, Wise, or a Big 4 multi-currency account) simplifies tracing.

- Use a regulated FX platform for conversions above AUD 50,000. Providers such as Wise for Business, OFX, and AirWallex are licensed in both jurisdictions and often beat bank spreads by 1–2%.

- Provide the required paperwork: certificate of incumbency, memorandum of association, shareholder passport copies, tax residency certificate (if available), and the latest management accounts. Having these ready shaves days off compliance checks.

4. Sequence the transfer for maximum tax efficiency

A common mistake is to wire profits in the same financial year they are earned, which can push you into a higher marginal tax bracket in Australia. Consider this timeline instead:

- FY1 (in the UAE)

- Close the financial year and calculate taxable profit.

- If you are a Qualifying Free Zone Person, ensure your income meets ‘Qualifying Income’ criteria to lock in the 0% rate.

- Early FY2

- Hold a board meeting to declare a dividend after the UAE return is filed.

- Apply to your UAE bank for a dividend remittance letter (some banks require it for sums above AED 500k).

- June–July FY2

- Transfer funds when the AUD is seasonally weak against the USD/AED peg, or use forward contracts to lock in a rate.

- Declare the dividend in your Australian tax return for FY2, avoiding the FY1 higher-income spike.

5. Protect your transfer from fees and FX slippage

| Transfer size | Best channel | Typical total cost* | Processing time |

|---|---|---|---|

| <$10,000 AUD | Wise personal | 0.7–1.0% | <24 h |

| $10k–$250k | OFX or AirWallex | 0.4–0.7% | 1–2 days |

| >$250k | Bank-to-bank with negotiated margin | 0.25–0.4% | 1–3 days |

*Includes SWIFT fee, FX margin, and receiving-bank fee. Figures are Dubai → Australia averages in 2025.

Tips to save more:

- Batch small dividends into quarterly transfers to minimise fixed SWIFT fees.

- Request “OUR” fee option so sending bank absorbs charges (some Aussie banks rebate incoming fees for premier clients).

- Avoid AED → AUD directly. Convert AED to USD first (1 AED is always 0.2722 USD), then USD to AUD. The two-step path often produces a better net rate.

6. Keep the ATO satisfied: reporting checklist

- Foreign Income Schedule (FIS) – declare gross dividend or profit share in AUD at the RBA published rate on the day you received the funds.

- FITO Worksheet – claim a credit for UAE CT paid (if any). Attach the UAE Federal Tax Authority payment receipt.

- CFC Statement – if your UAE company is caught, include attributable income even if no dividend was paid.

- FX Documentation – platform receipts, bank statements, and board minutes.

- Record retention – minimum five years. Digital copies are acceptable if legible.

The ATO initiated Operation Sunseeker in late 2024, targeting undeclared Middle East income flows. Expect data-matching between UAE banks and AUSTRAC to tighten further in 2025–26.

7. Common red flags and how to avoid them

- Circular transfers: Funds leave Australia, briefly touch a Dubai account, then return as “foreign profits”. This is classic GAAR territory.

- Cash deposits in UAE above AED 55,000 without source evidence. Banks file Suspicious Transaction Reports (STRs) that AUSTRAC can obtain.

- Multiple related-party loans from your UAE company to you personally. The ATO may treat them as unfranked dividends.

- Under-market FX rates on intercompany transfers. Arm’s-length principle applies even without a DTA.

8. Case study: Steven’s free-zone consultancy

Steven, a Perth-based IT consultant, set up a 100%-owned company in Dubai Internet City (a free zone). In calendar 2024 the company earned AED 1.2 million (≈ AUD 500k) profit. Here’s how he repatriated funds:

- Corporate tax: As a Qualifying Free Zone Person, 0% tax applied after substance test passed (two employees and dedicated office).

- Dividend declaration: Board resolution in February 2025 for AED 900k dividend.

- FX strategy: Locked USD → AUD forward at 0.70 using OFX; net spread 0.45%.

- Transfer: Two tranches of USD 100k each to his Macquarie AUD IBAN.

- ATO reporting: Declared AUD 285k dividend in his FY 2024-25 return; no FITO because 0% UAE CT.

- Outcome: Total transaction costs AUD 3,150; effective tax rate 37% marginal bracket in Australia only (no double taxation).

Frequently Asked Questions (FAQ)

Do I need an Australian bank account in my company’s name to receive dividends?

No. Dividends can be paid directly to the shareholder’s personal account. However, if multiple shareholders are involved, a nominee Australian bank account helps simplify reconciliations.

Is there a limit on how much money I can transfer out of the UAE?

There is no legal cap, but transfers above AED 100k prompt enhanced due-diligence checks at UAE banks.

Will the ATO tax me if I keep the profits in Dubai and don’t bring them home?

Possibly. Under CFC rules, “tainted” passive income can be attributed to you even if undistributed. Active business income can usually be deferred, but you still need to pass the active-income test.

Can I use crypto to move my money more cheaply?

Technically yes, but it raises AML concerns and can trigger CGT events in Australia. Mainstream banks may also refuse inbound transfers from crypto exchanges.

What about using a holding company in the Cayman Islands between Dubai and Australia?

Interposing another low-tax jurisdiction rarely improves your position without a DTA. The ATO’s Multinational Anti-Avoidance Law could still apply.

Ready to streamline your profit repatriation?

Dubai Invest specialises in end-to-end structuring for Australian entrepreneurs—company formation, banking, tax planning, and, crucially, cross-border cash management that keeps both UAE regulators and the ATO happy.

Book a free 30-minute strategy call today: https://dubaiinvest.com.au