How Australians Can Use Home Equity to Buy Property in Dubai

Many Australians build significant wealth in their home, but struggle to redeploy it into higher yielding global property. One increasingly common strategy is to use Australian home equity (via refinance or a top-up loan) to fund a Dubai deposit and costs, then buy either a ready property with immediate rent, or an off-plan asset with staged payments.

Because this involves two banking systems, two legal frameworks, foreign exchange, and Australian tax reporting, the difference between a “good idea” and a clean execution is usually deal-level planning. At Dubai Invest, our lead consultant Jomon Ulahannan brings real work and business experience in Dubai, helping Australian investors structure the funding pathway, shortlist the right assets, and coordinate on-ground steps.

What Is Home Equity and How Does It Work in Australia?

Home equity is the difference between your property’s current market value and what you still owe on your mortgage.

- If your home is worth $1,000,000 and your loan balance is $600,000, your equity is $400,000.

In practice, banks usually don’t let you borrow against 100% of that equity. A common benchmark is the 80% loan-to-value ratio (LVR) threshold before lenders mortgage insurance (LMI) may apply, but each lender and borrower profile is different.

A simplified way many Australians estimate “usable equity” is:

- Usable equity ≈ (Home value × 80%) − Current loan balance

Example:

- Home value: $1,000,000

- 80% of value: $800,000

- Current loan: $600,000

- Usable equity: ~$200,000

That usable equity can be accessed through:

- Refinancing (replacing your current loan with a larger one)

- Top-up / equity release with your existing lender

- Line of credit style facilities (less common than they used to be, and policy varies)

Can Australians Legally Use Home Equity to Invest Overseas?

Yes, Australians can generally borrow against Australian property and use the funds to invest overseas, including UAE property investment. The key is that legality is not the same as suitability.

What you must consider before you proceed:

- Your lender’s conditions: Some lenders ask what the funds are for, and may assess serviceability and risk differently for investment purposes.

- Responsible lending and cash flow buffers: You are increasing debt on your Australian balance sheet.

- Cross-border transfer and compliance: Large international transfers trigger bank and regulatory checks, and you need clean documentation (source of funds, purchase contract, ID verification).

- Australian tax reporting: Australian residents are typically taxed on worldwide income, so Dubai rental income still needs to be reported to the ATO (even if UAE tax is nil for many residential scenarios).

This is exactly where a consultation matters: you want the equity release, FX plan, purchase timeline, and ongoing costs to align, not collide.

Step-by-Step Process to Use Home Equity for Buying in Dubai

Step 1 – Property Valuation & Equity Assessment

Start by confirming two numbers:

- Current property value (bank valuation or independent appraisal)

- Current loan balance and product terms (rate, fixed period, break costs)

Then stress-test serviceability:

- What happens if your Australian interest rate rises?

- What happens if the Dubai property is vacant for 2 to 3 months?

Dubai Invest can help you model an investment plan, but your Australian broker or lender will confirm what you can actually access.

Step 2 – Refinancing or Top-Up Loan Approval

Once you decide the equity access method, allow time for:

- Loan assessment and conditional approval

- Valuation completion

- Formal approval and settlement

Timing matters because Dubai transactions can move quickly, especially for well priced ready properties.

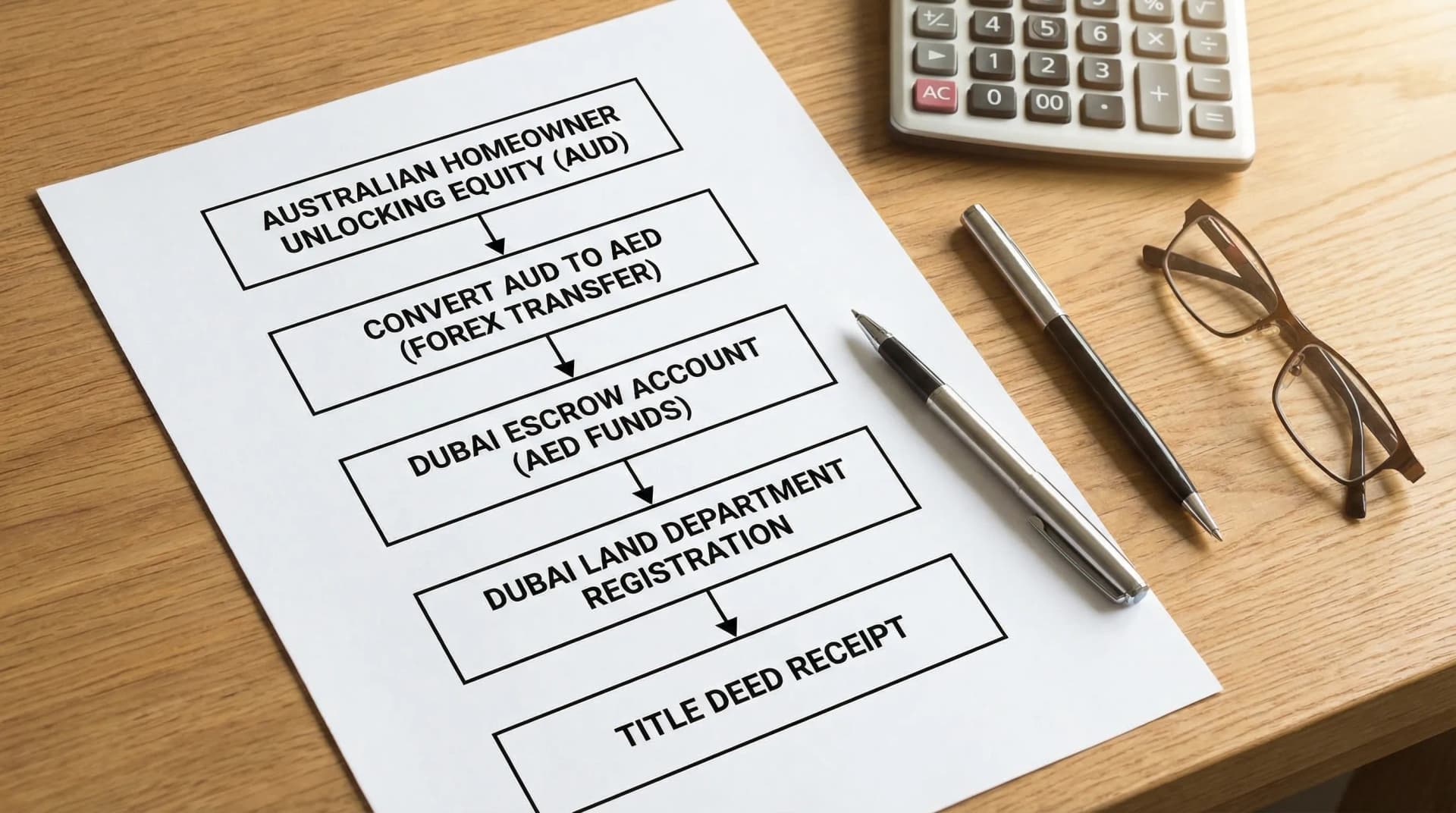

Step 3 – Currency Conversion & Fund Transfer to UAE

Your equity release will be in AUD, while Dubai property is priced in AED.

Key decisions include:

- Whether to convert a lump sum or stage conversions

- Whether to hedge FX risk (particularly for off-plan payment schedules)

- Which transfer rail you will use (bank wire vs specialist provider)

Dubai Invest frequently coordinates fund transfer timing alongside the developer or trustee deadlines, so you do not miss a reservation, escrow milestone, or transfer appointment.

Step 4 – Selecting the Right Dubai Property

This is where many equity-funded investors either win or leak returns.

Instead of starting with glossy marketing, underwrite the property around:

- Tenant demand (who rents here and why)

- Building-level service charges (they can materially change net yield)

- Liquidity (resale depth in that tower or community)

- Title type (freehold vs leasehold) and contract terms

If you decide to visit for inspections, consider using the trip to understand waterfront micro-markets properly (Marina, Bluewaters, Palm). Some investors even view the coastline from the water via a luxury yacht charter to compare access, marinas, and lifestyle drivers that influence premium rents.

Step 5 – Completing the Purchase in Dubai

The completion pathway depends on whether it is ready or off-plan, but typically includes:

- Reservation and initial deposit

- Sales and Purchase Agreement (SPA) review and signing

- KYC and source of funds checks

- Payment into the correct escrow or trustee channels

- Dubai Land Department (DLD) registration

- Title deed issuance (ready) or Oqood registration (off-plan)

Dubai Invest’s value in this stage is coordination, verification, and reducing “distance risk” for Australians buying remotely.

Why Dubai Is Attractive for Equity-Funded Investors

Dubai tends to appeal to equity-funded investors because it combines:

- Potentially higher gross yields than many Australian metro markets (deal and strategy dependent)

- No annual property tax and, in many residential contexts, no local tax on rental income (Australians still need to report income at home)

- Strong population growth and rental demand across multiple hubs

- A mature freehold framework for foreign buyers in designated zones

Equity funding can be particularly powerful if the Dubai asset generates income quickly (ready property), or if an off-plan payment plan matches your cash flow rather than forcing all capital upfront.

Cost Breakdown: What Australians Should Budget For

Your budget needs to cover more than the headline price. Below is a practical checklist style breakdown (exact fees vary by deal, provider, and structure).

| Cost item | Where it applies | What to know (high level) |

|---|---|---|

| Australian bank valuation, settlement and loan fees | Australia | Varies by lender and product, factor in timing |

| Interest costs on increased Australian debt | Australia | Biggest long-term cost driver, stress-test buffers |

| FX spread and transfer fees | Australia to UAE | Often underestimated, especially with staged off-plan payments |

| DLD transfer / registration fees | Dubai | Commonly budgeted at around 4% of purchase price (plus admin) |

| Agent / broker commission | Dubai | Often around 2% (terms vary) |

| Trustee / admin charges | Dubai | Applicable in many ready-market transfers |

| Service charges (strata style) | Dubai | Building and community dependent, impacts net yield |

| Property management | Dubai | Typically a percentage of rent, plus letting fees |

| Furnishing (if required) | Dubai | Especially relevant for short-term rental strategy |

A consultation is useful here because equity-funded buyers often want to know the real question: “How much cash do I need to deploy before the property is rent-ready?”

Risk Factors to Consider Before Leveraging Equity

Using equity can accelerate wealth creation, but it also magnifies mistakes. Key risks to assess:

- Interest rate risk in Australia: Your home loan is the funding engine.

- Currency risk (AUD to AED): FX can improve or hurt your entry cost and repatriated returns.

- Vacancy and rent variability: Underwrite conservative occupancy assumptions.

- Service charge inflation: Net yield can drop even if gross yield looks strong.

- Off-plan delivery risk: Delays and specification changes must be priced in.

- Regulatory and documentation friction: KYC and source of funds checks can slow timelines.

- Australian tax compliance: Record-keeping, FX conversion to AUD, deductions, and CGT planning.

If you want to reduce risk, the most practical step is to seek a deal-specific consultation that tests your numbers and your timelines before you transfer funds.

Off-Plan vs Ready Property – Which Suits Equity Investors?

Equity-funded Australians often split into two profiles: cash flow first (ready) or growth and staged payments (off-plan). Here is a practical comparison.

| Factor | Off-plan | Ready |

|---|---|---|

| Upfront cash required | Often lower upfront due to payment plans | Typically higher upfront to complete |

| Rental income | Usually starts at handover | Can start soon after settlement |

| Timeline risk | Higher (construction, handover timing) | Lower (existing asset) |

| Due diligence focus | Developer quality, escrow, SPA clauses | Building quality, tenants, service charges |

| Best fit for equity investors | Those who want staged funding and can wait | Those who want rent now to offset interest |

Dubai Invest can walk you through which option fits your equity release amount, repayment comfort, and investment horizon.

Case Study: Using $200K Equity to Build a Dubai Property Portfolio

This is an illustrative example to show how equity can be deployed. It is not financial advice.

Starting position (Australia):

- Usable equity released: $200,000 AUD

- Goal: Build a Dubai portfolio with diversification rather than a single high-ticket unit

- Strategy: Use off-plan payment plans to control two assets with staged cash calls

Assumptions (illustrative):

| Assumption | Value |

|---|---|

| Equity available | $200,000 AUD |

| FX rate | Assumed for modelling only (rate changes daily) |

| Target property type | 1-bedroom apartments in liquid rental areas |

| Hold period | 5+ years |

| Rental strategy | Long-term leasing to reduce operational volatility |

How the $200K could be deployed:

- Reserve Unit A and Unit B with staged payment plans

- Allocate capital to deposits, DLD style registration, and a buffer for future instalments

- Keep a contingency buffer for FX movements and Australian interest costs

Why the “two-unit” approach can work for equity investors:

- Diversifies vacancy risk (one unit vacant does not mean zero income)

- Improves resale flexibility (sell one, hold one)

- Lets you match cash calls to your income cycle, rather than paying 100% day one

The key is that this only works when the project, developer terms, service charge forecasts, and tenant demand are verified. This is where Jomon’s on-ground Dubai experience helps Australians avoid deals that look good on paper but underperform in net terms.

Next step: book a consultation

If you are considering using home equity to buy in Dubai, the highest value move is to validate your plan before you refinance or send funds. Dubai Invest can map your equity release timeline to a Dubai purchase timeline, shortlist properties that fit your risk profile, and coordinate documentation, FX, and settlement. Book a consultation with jomon