How Off-Plan Mortgages Work with 80/20 Payment Plans in Dubai

Off-plan property is one of the most popular investment options in Dubai, particularly for Australian buyers looking for flexible payment structures, entry into new developments, and strong potential for capital appreciation before handover.

However, combining a mortgage with an 80/20 payment plan introduces a more complex structure. Factors such as bank financing rules, developer payment schedules, escrow account regulations, property valuation timing, and non-resident eligibility all play a crucial role.

This guide breaks down how off-plan mortgages work in Dubai, what Australian investors need to prepare for, and why seeking professional advice before paying a booking deposit can help avoid costly mistakes.

What Is an Off-Plan Property in Dubai?

An off-plan property is a property purchased before it is completed. You are buying from a developer based on approved plans, specifications, floor plans, and construction milestones.

In Dubai, off-plan real estate is popular because buyers can often access:

- Lower entry prices compared with completed units in the same area

- Flexible developer payment plans

- New buildings with modern amenities

- Potential capital appreciation before completion

- Early access to high-demand communities and launches

For Australian investors, off-plan can be attractive because payments are usually spread over time instead of paid fully upfront. However, off-plan is not risk-free. You are relying on the developer’s ability to deliver the project, the market holding up, and your funding plan staying on track.

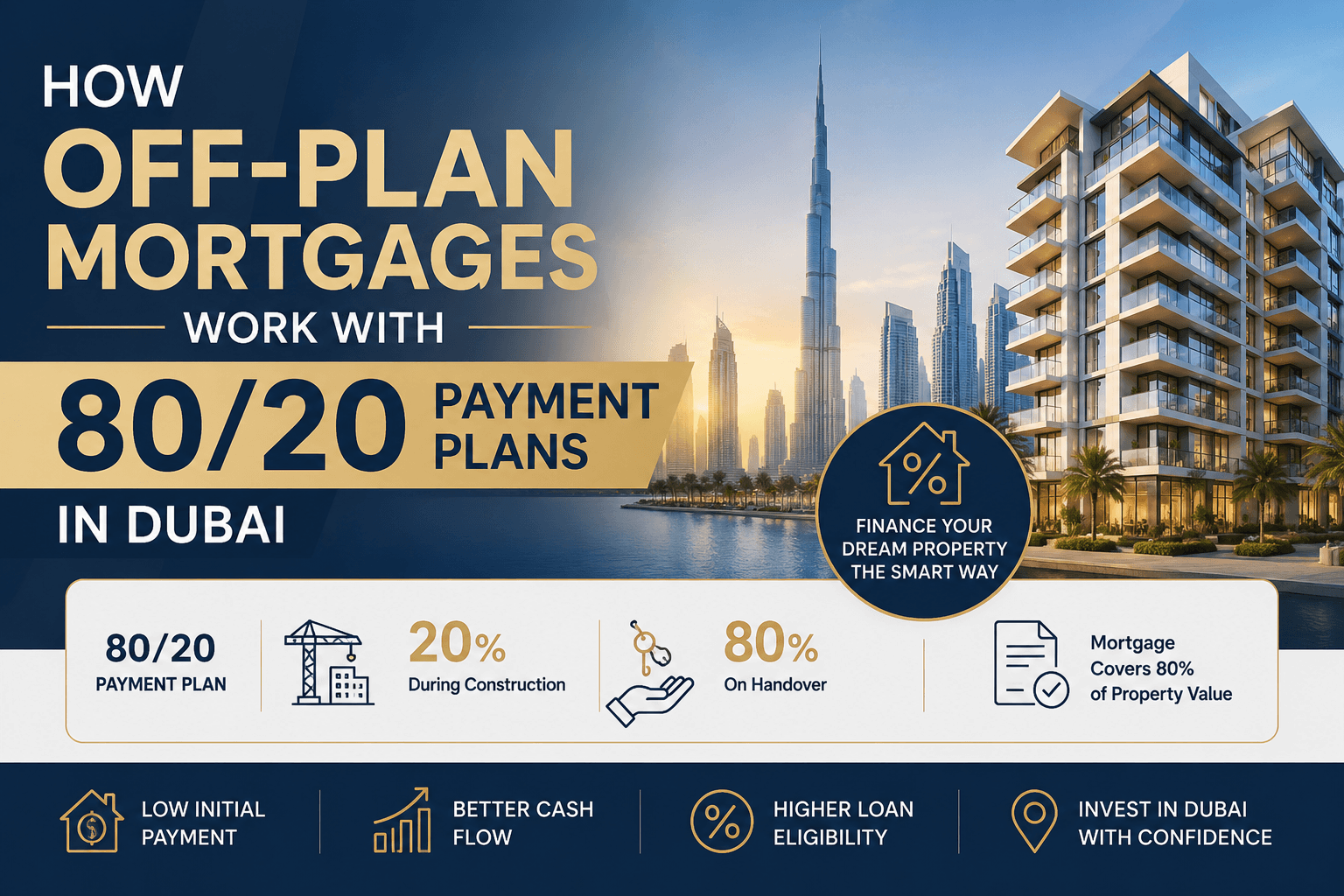

What Is the 80/20 Payment Plan in Dubai Real Estate?

An 80/20 payment plan means the buyer pays 80% of the property price during construction and the remaining 20% on handover.

A typical structure may look like this:

| Stage | Typical payment | What it means |

|---|---|---|

| Booking | 5% to 20% | Paid to reserve the unit |

| During construction | Instalments up to 80% | Paid according to construction or date-based milestones |

| Handover | Final 20% | Paid when the property is ready and transferred |

The exact instalment schedule depends on the developer and project. Some plans are linked to construction progress, while others are fixed by date.

How Off-Plan Mortgages Work in Dubai

Off-plan mortgages in Dubai do not work exactly like ready-property mortgages.

For a completed property, the bank can value the unit, approve the buyer, register the mortgage, and release funds at transfer. For off-plan, the bank may not be willing to finance the purchase until the project reaches a specific stage or is close to completion.

In practical terms, the mortgage may work in one of three ways:

- The buyer pays early instalments directly and uses the mortgage for the final handover amount.

- The bank finances approved construction-stage payments on selected developer projects.

- The bank steps in once the project reaches a required completion percentage, subject to valuation and final approval.

Bank involvement usually includes income assessment, credit checks, property valuation, final offer approval, mortgage registration, and controlled fund release to the developer or escrow account.

For Australians, the key point is simple: do not assume the bank will fund every instalment from day one. Many off-plan purchases require a strong cash-flow plan before the mortgage becomes available.

Can You Get a Mortgage for Off-Plan Properties?

Yes, you can get a mortgage for off-plan properties in Dubai, but not every project, developer, or buyer will qualify.

Banks are generally more comfortable financing off-plan when:

- The developer is approved by the bank

- The project is registered with Dubai Land Department or the relevant authority

- The project has an official escrow account

- Construction has reached the bank’s required stage

- The buyer meets income, debt, and documentation requirements

Some developers have bank partnerships or mortgage tie-ups. These can make the process smoother, but they do not guarantee approval. The bank still assesses the buyer independently.

This is where a consultation is valuable. A project may look attractive, but if the mortgage timing does not match the payment plan, the investor can face a funding gap.

Eligibility Criteria for Off-Plan Mortgages in UAE

Eligibility depends on the lender, your residency status, income type, and the project itself.

For Australian investors, banks commonly look at:

- Income: Stable salary, business income, or investment income, usually supported by bank statements and tax documents.

- Credit profile: UAE residents may be assessed through AECB records. Non-residents may need to show overseas credit history and clean bank conduct.

- Residency status: UAE residents may have access to more lender options. Non-residents can still qualify, but loan-to-value ratios may be lower.

- Age and loan tenor: Lenders assess age at loan maturity and repayment capacity.

- Debt-to-income ratio: Existing mortgages, personal loans, credit cards, and business liabilities affect approval.

- Documentation: Passport, proof of address, income proof, bank statements, property documents, and source-of-funds evidence are usually required.

Self-employed Australians should prepare earlier. Banks often ask for business financials, tax returns, company ownership records, and longer banking history.

Dubai Invest helps Australian buyers prepare bank-ready files before committing to a project, reducing the risk of delays after the deposit is paid.

Step-by-Step Process to Buy Off-Plan Property with Mortgage

The process should be planned before you reserve the unit. A smooth purchase is usually about sequencing.

- Define your budget and funding split: Decide how much will come from cash, Australian home equity, savings, business income, crypto conversion, or UAE mortgage.

- Get a mortgage pre-assessment: Speak to a mortgage advisor before paying a booking fee, especially if you are a non-resident buyer.

- Shortlist bank-acceptable projects: Focus on developers and projects that have a realistic pathway to finance.

- Reserve the property: Pay the booking amount only after verifying the developer, project registration, and payment destination.

- Review the SPA: Check payment milestones, delay clauses, handover terms, assignment rules, and default consequences.

- Complete bank application: Submit income documents, bank statements, identity documents, and property details.

- Pay construction instalments: Make staged payments according to the 80/20 plan, usually into the approved escrow account.

- Finalise mortgage before handover: The bank completes valuation, final approval, mortgage registration, and disbursement where applicable.

- Complete handover: Pay the remaining balance, complete snagging, receive handover documents, and arrange leasing or property management.

Advantages of 80/20 Payment Plans for Investors

An 80/20 payment plan can work well when matched with the right investor profile.

The main advantages include:

- Staged cash flow: Payments are spread across construction instead of paid upfront.

- Lower immediate capital pressure: You can enter the project with a booking deposit rather than full purchase price.

- Potential capital growth: If the area and project perform well, the property may appreciate before handover.

- Handover funding flexibility: The final 20% may be covered by cash, mortgage, refinance, or sale proceeds, depending on your plan.

- Remote investment suitability: Many developers support digital documentation and overseas buyer processes.

However, 80/20 is not automatically better than 60/40, 70/30, or post-handover plans. The right structure depends on your income, mortgage eligibility, currency strategy, and exit timeline.

Risks of Off-Plan Property Investment in Dubai

Off-plan property can be profitable, but it carries risks that ready property does not.

Common risks include:

- Construction delays that extend your payment and rental-income timeline

- Market fluctuations before completion

- Developer delivery or quality concerns

- Mortgage approval changing before handover

- AUD to AED currency movement increasing your effective cost

- Service charges being higher than expected after handover

- Resale restrictions before a certain percentage is paid

Mitigation starts before the deposit. Check the developer’s delivery record, confirm project registration, verify escrow details, review the SPA, and stress-test your cash flow.

Best Developers Offering 80/20 Payment Plans in Dubai

Payment plans change frequently, and not every project from a major developer will offer 80/20 terms. Still, Australian investors often see 80/20 or similar structured plans from established Dubai developers.

Developers to watch include:

- Emaar Properties

- DAMAC Properties

- Nakheel

- Sobha Realty

- Meraas

- Dubai Properties

- Ellington Properties

- Danube Properties

The developer name alone is not enough. You still need to assess location, price per square foot, service charges, payment schedule, escrow status, handover timing, and resale liquidity.

Differences Between Mortgage vs Developer Payment Plans

A mortgage and a developer payment plan are different funding tools. Many investors confuse the two.

| Feature | Bank mortgage | Developer payment plan |

|---|---|---|

| Provider | UAE bank or lender | Property developer |

| Approval required | Yes, based on income and credit | Usually lighter buyer checks, subject to developer policy |

| Security | Mortgage registered against property | Contractual instalment obligation under SPA |

| Interest | Usually interest or profit rate applies | Often interest-free during construction, but price may reflect the plan |

| Timing | Often available near completion or on approved projects | Starts from booking and continues through construction |

| Flexibility | Subject to bank rules and valuation | Subject to developer terms |

| Main risk | Rate changes, approval conditions, valuation gaps | Payment default, delays, limited financing support |

A developer payment plan helps you pay the developer over time. A mortgage is external financing from a bank. In some cases, they work together. In others, they do not align.

Before signing, confirm whether your mortgage can realistically cover the handover payment or any remaining instalments.

Hidden Costs in Off-Plan Property Purchases

The advertised property price is not the full cost.

Australian buyers should budget for:

- Dubai Land Department fees, commonly 4% of the purchase price

- Oqood or off-plan registration fees where applicable

- Administrative and trustee fees

- Mortgage valuation fees

- Mortgage registration fees if bank finance is used

- Bank arrangement or processing fees

- Legal or conveyancing review costs

- Currency transfer and FX margin costs

- Service charges from handover onward

- Snagging, furnishing, and property management costs

These costs can materially change your net return. For example, a strong headline yield may look less attractive after service charges, vacancy, management fees, and currency conversion are included.

This is why Dubai Invest encourages deal-level modelling rather than relying on brochure numbers.

Tips for Securing the Best Off-Plan Mortgage Deal

The best mortgage deal is not always the lowest advertised rate. It is the loan that fits your project, payment plan, residency status, and long-term investment strategy.

Practical tips include:

- Get pre-assessed before reserving a unit

- Compare multiple banks instead of relying only on the developer’s suggested lender

- Keep clean bank statements for at least six months

- Avoid taking on new debt before approval

- Prepare source-of-funds documents early

- Check whether the bank finances off-plan, near-handover only, or only selected developers

- Model fixed, variable, and Islamic finance options where available

- Plan AUD to AED transfers before each instalment date

For Australians, timing can be the difference between a smooth settlement and a stressful funding gap. Dubai Invest can assist with mortgage introductions, documentation handling, money transfer planning, and remote purchase support.

Conclusion – Is an 80/20 Off-Plan Mortgage Right for You?

An 80/20 off-plan mortgage strategy can be a smart way to invest in Dubai, but only if the payment plan, mortgage timing, developer quality, and your cash flow all work together.

It may suit you if you have stable income, sufficient cash for early instalments, a clear handover funding plan, and a medium to long-term investment horizon. It may not suit you if you need immediate rental income, maximum certainty, or full bank funding from the start.

Before paying a booking deposit, get advice specific to your situation. Dubai property investment is highly project-specific, and non-resident mortgage rules can vary between banks.

Book a consultation with Dubai Invest to review your budget, project shortlist, mortgage eligibility, and payment plan. With Jomon’s Dubai job experience, business experience, and local market network, Australian investors can make clearer decisions before committing capital.

Frequently Asked Question

What is an off-plan property in Dubai?

An off-plan property is a real estate unit that is purchased before construction is completed, usually offered at lower prices with flexible payment plans.

How does the 80/20 payment plan work in Dubai?

The 80/20 payment plan typically means 80% of the property price is paid during construction in installments, and the remaining 20% is paid upon handover.

Can I get a mortgage for an off-plan property in Dubai?

Yes, but mortgage approval depends on the developer, project stage, bank policies, and your eligibility as a resident or non-resident buyer.

Do banks finance the 80/20 payment plan?

Banks may partially finance off-plan properties, but in most cases, mortgage disbursement happens closer to handover rather than during early construction stages.

When does the mortgage start in an off-plan purchase?

In most cases, mortgage repayments begin closer to the handover stage when the property is completed and valuation is finalized.

What are the eligibility requirements for Australians?

Australian buyers typically need valid income proof, good credit history, passport documents, and may need a higher down payment as non-residents.