Investing in Dubai Property from Australia: Complete Guide

Investing in Dubai property from Australia is increasingly attractive in 2026 because Dubai can offer stronger gross rental yields than many Australian capital-city markets, no UAE personal income tax on residential rental income, and a purchase process that can often be managed remotely with the right local support.

For Australian investors, the opportunity is not simply buying overseas property. It is choosing the right asset, structure, funding route, and rental strategy before sending funds across borders.

Key 2026 investor signals:

- Rental yields: commonly around 5% to 8%+ gross, depending on area, building, service charges, and rental model

- UAE tax position: 0% personal income tax on the UAE side for most individual investors

- Entry price range: many investors begin around AED 500,000 to AED 1 million for studios or compact apartments, with higher budgets for prime, villas, and Golden Visa strategies

Why Australians Are Investing in Dubai Property in 2026

Strong Rental Yields vs Australian Cities

Australian investors often compare Dubai with Sydney, Melbourne, Brisbane, and Perth due to the yield gap. While Australia focuses on long-term capital growth, Dubai can offer stronger rental income depending on location, property type, and management.

For detailed insights, see Dubai Invest’s guide on rental yields by area. The key point: gross yield is only the starting point—net return after service charges, vacancy, and management costs matters most.

Currency Advantage & AUD–AED Dynamics

The AED is pegged to the USD, so Australian investors are exposed to AUD/USD movements. A stronger AUD improves buying power, while a weaker AUD increases costs for deposits and repayments. Currency planning is essential, especially for off-plan purchases.

Tax Efficiency (Australia vs UAE)

Dubai generally has no personal income tax on rental income and no annual property tax. However, Australian tax residents must declare global income to the ATO, including overseas property gains. Proper structuring before purchase is crucial.

Investor-Friendly Regulations in Dubai

Dubai offers foreign ownership in freehold zones regulated by the Dubai Land Department and RERA. Systems like Oqood (off-plan) and title deeds (ready properties) ensure clearer ownership, but due diligence on developers and escrow accounts is still essential.

Global Trends & Capital Flow Impact

In 2026, Dubai continues to attract global investors due to its location, infrastructure, tourism, and business growth. For Australians, it offers both rental income potential and portfolio diversification, backed by strong macroeconomic demand.

Is Dubai Safe for Investment in 2026?

UAE’s political stability in the Middle East

The UAE is considered one of the most stable and business-friendly economies in the region. Its policies strongly support foreign investment, tourism, infrastructure growth, and business setup. This stability helps maintain tenant demand, investor confidence, and long-term property value.

Regional conflicts (2026 context)

While regional tensions exist, investors should assess risk calmly rather than react to headlines. The UAE follows a diplomacy-driven and diversified economic model, with Dubai supported by trade, tourism, finance, logistics, and technology not a single industry.

Dubai real estate resilience during uncertainty

Dubai continues to attract global capital during uncertain times due to its liquidity, strong regulation, international tenant base, and ease of doing business. However, performance still depends on selecting the right property and location.

Why investors choose Dubai during global instability

Dubai offers rental income potential, tax advantages (on UAE side), global connectivity, lifestyle benefits, and residency pathways. For overseas buyers like Australians, working with local experts helps reduce risk and ensure better decision-making in cross-border investments.

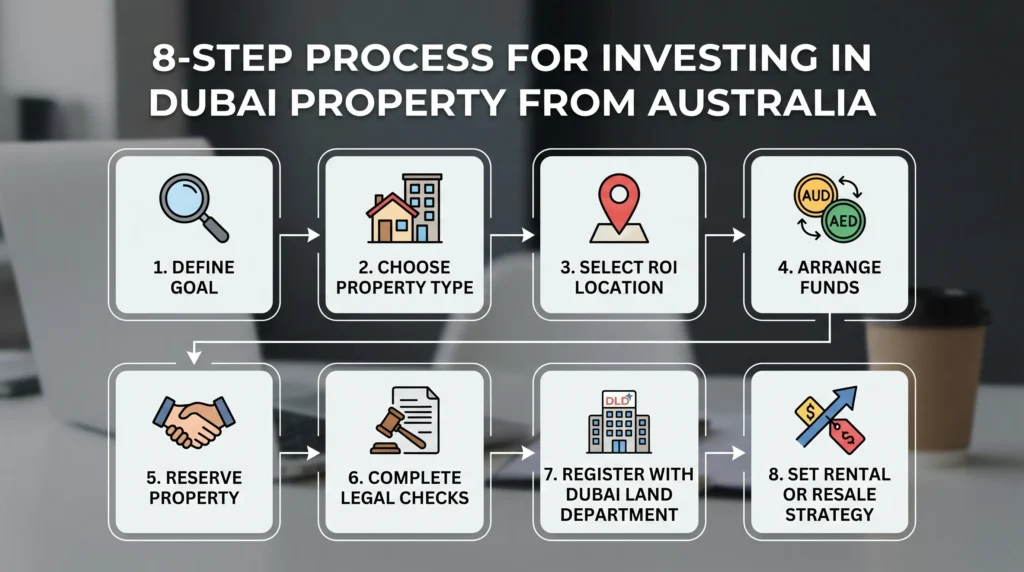

Step-by-Step Process to Invest in Dubai Property from Australia

Step 1: Define your investment goal

Start with the outcome. Are you targeting passive rental income, capital growth, Golden Visa eligibility, a future relocation base, or portfolio diversification? Your goal determines the area, property type, budget, financing route, and rental strategy

Step 2: Choose the right property type

Studios and 1-bedroom apartments can suit yield-focused investors. Larger apartments may attract families or professionals. Villas and townhouses may suit lifestyle and long-term capital-growth strategies. Commercial property requires deeper tenant and lease analysis

Step 3: Select location based on ROI

Do not buy Dubai as a single market. Buy a specific unit in a specific building within a specific micro-location. Compare tenant demand, service charges, resale liquidity, transport access, and upcoming supply

Step 4: Arrange financing or funds

You can buy with cash, a UAE non-resident mortgage, Australian home equity, developer payment plans, or a combination. Before reserving a property, confirm deposit timing, bank requirements, source-of-funds documents, and currency transfer strategy

Step 5: Reserve property (booking process)

The booking process usually involves paying a reservation amount or deposit and signing initial documentation. Before transferring money, verify the developer or seller, check escrow details for off-plan property, and confirm whether the payment is refundable or non-refundable

Step 6: Legal checks & documentation

Important checks include title or Oqood verification, developer registration, escrow account validation, sales agreement review, buyer KYC, source-of-funds evidence, and power of attorney wording if you are buying remotely

Step 7: Property registration (Dubai Land Department)

Property registration is completed through the Dubai Land Department process. For off-plan purchases, Oqood registration is typically used. For completed properties, title deed transfer is the key ownership milestone

Step 8: Rental or resale strategy

After purchase, decide whether to lease long-term, operate as a holiday home, hold for capital growth, refinance later, or prepare for resale. Your strategy should be documented before completion so the property does not sit vacant

Best Property Types for Australian Investors

Apartments (Studio, 1BR, 2BR)

Apartments are often the most practical entry point for Australian investors because they can offer lower purchase prices, broader tenant demand, and easier remote management. Studios can suit budget and yield strategies, while 1-bedroom and 2-bedroom apartments can offer stronger tenant depth in selected communities.

Useful apartment resources include studio apartments for sale in Dubai, Dubai 2 bedroom apartments for sale, flats for sale in Dubai, and serviced apartments in Dubai.

Villas & Townhouses

Villas and townhouses appeal to families, lifestyle buyers, and long-term investors. They usually require higher budgets and may have different maintenance and community-fee considerations, but they can benefit from limited land-style supply in well-planned communities.

Off-plan vs Ready Properties

Off-plan property can offer staged payment plans and early-cycle pricing, but investors must assess developer track record, escrow protection, completion timelines, and resale restrictions. Ready property can generate rent sooner and is usually easier to inspect, value, and finance.

Commercial Properties (offices, retail, warehouses)

Commercial property can offer contract-driven income, but the due diligence is more complex. You need to understand lease terms, tenant quality, vacancy risk, VAT treatment, service charges, and liquidity before buying.

Hotel Apartments & Short-term rentals

Hotel apartments and short-term rentals may suit investors seeking higher gross income potential, especially in tourism-heavy locations. The trade-off is higher management complexity, operator fees, furnishing costs, seasonality, and regulatory requirements.

Top Areas in Dubai for Australian Investors (2026)

High rental yield areas

Yield-focused investors often review communities such as Jumeirah Village Circle, Dubai Silicon Oasis, Dubai Sports City, International City, and selected parts of Dubai South. The best opportunities are usually building-specific rather than area-wide.

Affordable investment zones

Affordable zones can help investors enter the market at lower price points. These may include JVC, Dubai South, Al Furjan, Dubai Land communities, and other developing residential districts. Lower entry cost is useful, but investors should still test liquidity, service charges, and tenant demand.

Premium luxury investment areas

Premium investors often consider Downtown Dubai, Dubai Marina, Palm Jumeirah, Dubai Hills Estate, Dubai Creek Harbour, and Business Bay. These areas can offer stronger global recognition and lifestyle appeal, although purchase prices and service charges may be higher.

Emerging hotspots

Emerging hotspots in 2026 include areas supported by infrastructure, employment hubs, masterplans, and population growth. Dubai South, Expo City-linked districts, Dubai Creek Harbour, and selected master-planned communities deserve careful review. See Dubai Invest’s guide to emerging Dubai property hotspots for more detail.

ROI, Rental Yield & Capital Growth Expectations

Average rental yields in Dubai

Dubai rental yields often sit around 5% to 8%+ gross, with some compact apartments and high-demand locations exceeding that range. Net yield is lower after service charges, vacancy, property management, maintenance, insurance, and currency costs.

| Investment factor | What to check | Why it matters |

|---|---|---|

| Gross rent | Comparable leases and current listings | Shows income potential |

| Service charges | Building and community fees | Can reduce net yield materially |

| Vacancy | Area and unit demand | Affects real cash flow |

| Resale liquidity | Transaction volume and buyer demand |

Helps exit strategy |

Short-term vs long-term rental ROI

Short-term rentals can generate higher gross income in tourist and business districts, but they involve furnishing, licensing, operator fees, cleaning, and occupancy risk. Long-term rentals are often simpler and more predictable for remote Australian landlords.

Capital appreciation trends

Capital growth depends on purchase timing, supply, infrastructure, developer quality, and area maturity. In a fast-moving market, buying a poor unit in a good area can still underperform. Deal-level modelling is essential.

Case study (optional internal blog link)

For a practical example of yield-led execution, read Dubai Invest’s case study on how a Sydney couple built a 9% net yield Dubai short-term rental portfolio. Treat case studies as examples, not guarantees.

Financing Options for Australians

Cash vs mortgage investment

Cash buyers can move quickly, negotiate strongly, and avoid interest-rate risk. Mortgage buyers can preserve liquidity and use leverage, but must account for approval timelines, valuation risk, deposit requirements, and currency exposure.

Non-resident home loans in Dubai

Australian buyers may be eligible for non-resident home loans in the UAE, subject to income, documents, bank policy, property type, and valuation. Learn more about non-resident home loans in Dubai before relying on finance.

Documents required for mortgage approval

Common documents include passport, proof of address, bank statements, income evidence, tax records for self-employed applicants, credit history, liabilities, and source-of-funds evidence. For more detail, see Dubai mortgage pre-approval documents Australians need.

Using equity from Australian property

Some Australians use Australian home equity to fund a Dubai purchase or deposit. This can improve speed and flexibility, but it links Australian debt, FX risk, and overseas property performance. Dubai Invest’s guide on using home equity to buy property in Dubai explains the process.

Tax Implications for Australian Investors

UAE tax benefits (0% income tax context)

For most individual residential property investors, Dubai does not impose UAE personal income tax on rental income. There is generally no annual property tax in the Australian sense and no standard UAE capital gains tax for individuals selling residential property.

Australian tax obligations (ATO rules)

Australian tax residents generally need to report worldwide rental income and capital gains to the ATO. Income and expenses usually need to be converted into AUD with proper records. Refer to the ATO guidance on foreign income and seek professional advice.

Double taxation considerations

Because the UAE often charges no personal income tax on this income, the Australian side may become the main tax issue for Australian residents. Treaty positions and tax residency rules can be technical, so do not rely on generic online summaries.

Repatriation of rental income

Rental income can usually be transferred from Dubai to Australia through banks or regulated FX providers, subject to KYC, AML, bank documentation, and Australian reporting. Keep tenancy contracts, Ejari records, statements, invoices, and transfer confirmations.

For related reading, see Dubai Invest’s guides on ATO obligations when investing in Dubai property and how the ATO may detect Dubai property income.

Risks of Investing in Dubai Property (and How to Mitigate Them)

Market fluctuations

Dubai property prices can move quickly. Mitigate this by avoiding hype-based buying, reviewing comparable transactions, stress-testing yield, and holding with a realistic timeframe.

Off-plan project delays

Off-plan projects can face construction, approval, or handover delays. Reduce risk by checking developer history, escrow details, SPA clauses, and project registration. Start with the guide on how to verify a Dubai developer.

Currency risk (AUD vs AED)

Currency movements can affect purchase price, staged payments, mortgage repayments, and repatriated income. Consider staged conversion, forward contracts where suitable, and clear FX planning.

Developer credibility risks

Not all developers, brokers, or projects are equal. Avoid pressure sales, unrealistic guaranteed returns, unclear escrow details, and vague handover promises. See buying off-plan red flags Australians should watch.

Liquidity and exit risks

Some properties are easier to sell than others. Before buying, check resale transaction volumes, competing supply, buyer demand, and whether the unit type is attractive to both tenants and future buyers.

Can You Invest Remotely from Australia?

Remote property buying process

Yes, many Australian investors can complete much of the Dubai buying process remotely. This usually involves digital shortlisting, video inspections, reservation documents, KYC, international transfers, POA where needed, and registration coordination.

Power of Attorney (POA)

A POA can allow a trusted representative to sign or complete certain steps in Dubai. The wording must match the required transaction and authority. Dubai Invest’s Power of Attorney for Dubai property guide explains setup and common mistakes.

Virtual property tours & digital transactions

Virtual tours can help, but they should not replace due diligence. Request building videos, floor-plan checks, view confirmation, service-charge history, comparable transactions, and community condition evidence.

Managing property remotely

Remote management is possible with a professional property manager, clear reporting, rent collection processes, maintenance approvals, and tax documentation. The goal is to make the investment passive without losing control.

Golden Visa & Residency Through Property Investment

Eligibility criteria

Dubai property investment can support residency pathways if eligibility conditions are met. For many investors, the 10-year Golden Visa is the key long-term residency route, but requirements should be confirmed before purchase.

Property value requirements

The commonly discussed real estate route for a UAE Golden Visa requires qualifying property investment of at least AED 2 million, subject to current rules and documentation. Always verify whether your selected property, payment status, and title documents qualify.

Benefits for Australians

Potential benefits include long-term renewable residency, family sponsorship options, easier UAE banking and local administration, and flexibility for business or lifestyle planning.

Costs Involved in Buying Property in Dubai

Dubai Land Department fees

The major buyer cost is commonly the Dubai Land Department transfer fee, often 4% of the property value. Off-plan and ready transactions can involve different registration steps, so confirm fees for the specific deal.

Agent fees

On secondary-market purchases, agent commission is commonly around 2% plus VAT, though this can vary by transaction. For developer sales, commission treatment may differ.

Service charges

Service charges are ongoing building and community costs. They can materially affect net yield, especially in towers with extensive amenities or premium locations. Review the building’s current and historical service charges before buying.

Maintenance & hidden costs

Budget for maintenance, insurance, furnishing, chiller or utility deposits, property management, vacancy, bank fees, FX costs, mortgage registration if borrowing, and resale costs. A consultation helps convert headline ROI into a realistic net-return model.

Exit Strategy – Selling Your Dubai Property

When to sell

Sell based on strategy, not emotion. Common triggers include reaching a target capital gain, weakening rental demand, better opportunities elsewhere, Golden Visa or residency changes, or upcoming supply that may pressure prices.

Capital gains considerations

The UAE may not impose a standard personal capital gains tax for individual residential sellers, but Australian tax residents may have CGT obligations in Australia. Keep acquisition documents, improvement invoices, loan statements, and sale records.

Repatriating funds to Australia

Sale proceeds can generally be repatriated after mortgage clearance, NOC processing, transfer completion, and bank compliance. Plan FX timing and documentation early. Dubai Invest’s guide on selling your Dubai property as a non-resident and repatriating funds is a useful next step.

Conclusion: Investing in Dubai Property from Australia in 2026

Investing in Dubai property from Australia can be a strong strategy in 2026 for investors seeking higher rental yields, UAE-side tax efficiency, international diversification, and potential residency benefits. But the result depends on execution.

The most important decision is not only which property to buy. It is whether your budget, ownership structure, funding plan, tax position, remote-management setup, and exit strategy all work together. That is why a consultation before paying a deposit can save time, reduce risk, and help you avoid costly mistakes.

Frequently Asked Questions

Can Australians buy property in Dubai?

Yes. Australians can buy property in designated freehold areas in Dubai, subject to standard KYC, source-of-funds checks, documentation, and registration requirements.

What is the minimum investment required?

Entry-level properties typically start around AED 500,000–1,000,000+, depending on location, type, fees, and financing

Is Dubai property tax-free?

Dubai has no personal income tax on rental income and no annual property tax like Australia. However, Australian tax residents must still report income and gains to the ATO

Is 2026 a good time to invest?

It can be, if you focus on net yield, developer quality, service charges, liquidity, and currency risk—not just market headlines

How safe is Dubai for investment?

It is a regulated and stable market, but risks still exist around pricing cycles, liquidity, currency, and individual projects

Can I buy from Australia without travelling?

Yes. Many purchases can be completed remotely using digital processes, verified payments, and Power of Attorney if needed